Course Content

Course Content

Uncategorized

About Course

FRM Lessons

Course Content

Chapter 1 – The Building Blocks of Risk Management

This chapter provides FRM exam candidates with a comprehensive foundation in risk management, covering the historical development of the field, key building blocks, and modern frameworks used by financial institutions. Across 12 lessons, candidates will learn how to identify, measure, and manage risk, while also understanding the limitations of traditional models and the importance of adapting to structural change, human behavior, and innovation.

Topics include the history of risk management, fundamental building blocks, typologies of risk, the risk management process, identifying knowns and unknowns, expected and unexpected loss, risk factor decomposition, the shift from tail risk to systemic risk, human agency and conflicts of interest, methods of risk aggregation, balancing risk and reward, and enterprise risk management.

By the end of this chapter, FRM Part I candidates will have a clear, structured understanding of how risk management evolved, why different risks must be managed through a unified framework, and how modern approaches such as ERM, stress testing, and data science shape today’s risk practices.

-

1. Risk Management Historical Timeline

11:17 -

2. Building Blocks of Risk Management & Typologies of Risk

05:05 -

3. Typologies of Risk

09:11 -

4. The Risk Management Process

08:01 -

5. Identifying Risk – Knowns and Unknowns

06:41 -

6. Expected Loss, Unexpected Loss & Tail Loss

05:56 -

7. Risk Factor Breakdown

03:12 -

8. Structural Change – From Tail Risk to Systemic Risk

03:32 -

9. Human Agency and Conflict of Interest

04:04 -

10. Risk Aggregation

05:52 -

11. Balancing Reward & Risk

03:30 -

12. Enterprise Risk Management (ERM)

03:14

Chapter 2 – How Do Firms Manage Financial Risk

This lesson introduces FRM exam candidates to the historical evolution of risk management. We trace the development of risk management from ancient practices of mitigating uncertainty, through the rise of probability theory in the 1600s, to modern regulatory frameworks. The timeline highlights four key dimensions: advancements in theory, actions to mitigate risk, shocks that raised awareness, and the growth of regulation.

By understanding this big picture, FRM Part I candidates can better appreciate how risk management is both an old craft and a young science—and why today’s profession continues to evolve in response to global events and regulatory changes.

This video is part of a full FRM preparation series designed to provide clear explanations of core concepts tested in the FRM exam.

-

1. The Modern Imperative to Manage Risk

05:20 -

2. Risk Appetite

03:05 -

3. Risk Mapping & Management

05:55 -

4. Rightsizing Risk Management

03:56 -

5. Risk Transfer Tools

05:34 -

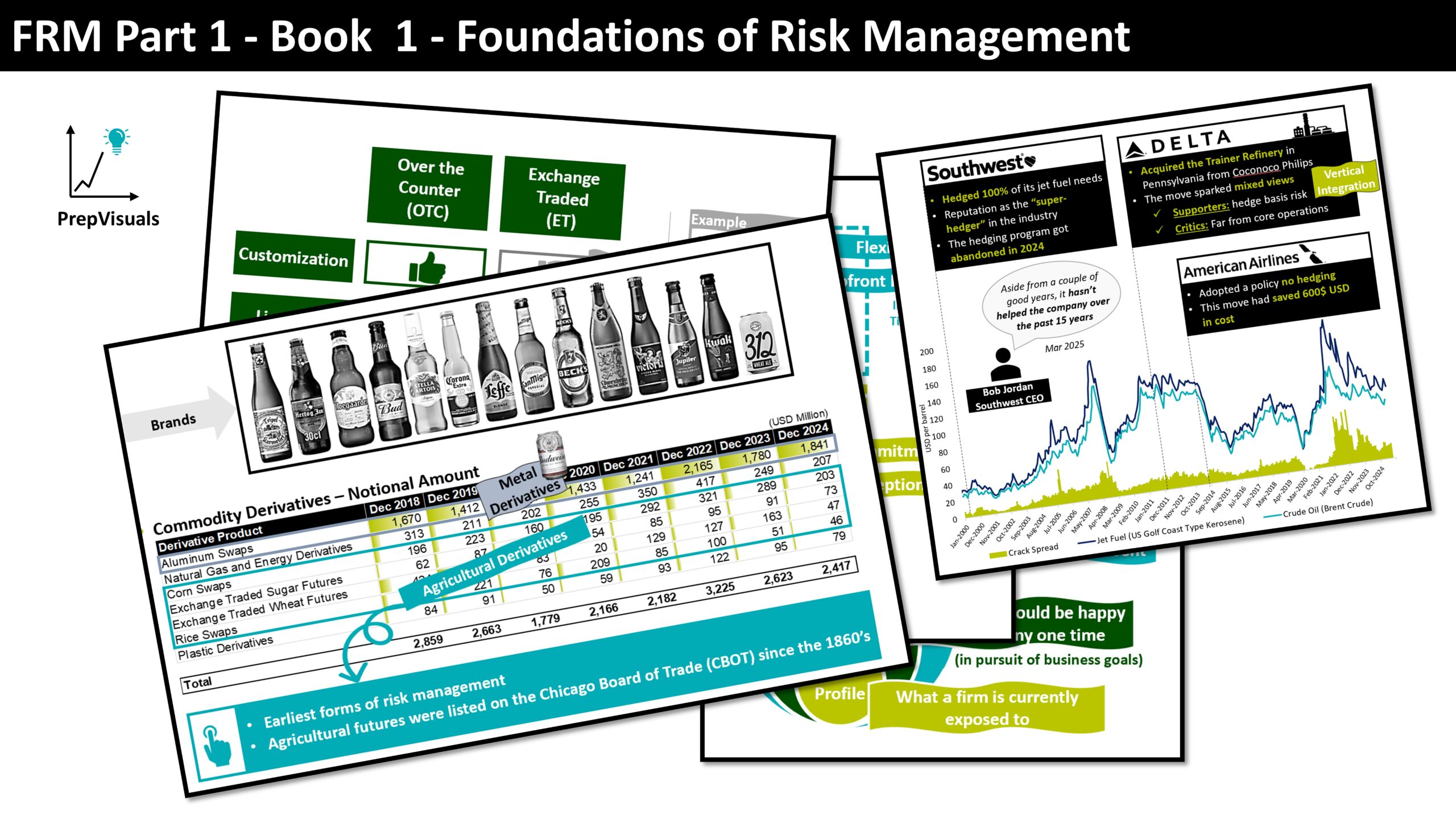

6. Case Study – Anheuser Busch

04:56 -

7. Case Study – Airline Industry

04:26 -

8. Case Study – McDonald’s

03:57 -

9. Case Study – Metalgesellschaft

10:18

Chapter 3: The Governance of Risk Management

This chapter provides a structured understanding of how modern financial institutions design, oversee, and enforce risk governance. Starting with the lessons of major corporate failures and global financial crises, we follow the evolution of regulatory reform — from Sarbanes-Oxley and Comply-or-Explain, to Dodd-Frank, SREP, and Basel III.

We break down the architecture of governance — from the Board of Directors and senior management to the Chief Risk Officer, Chief Auditor, and the three lines of defense — showing how risk appetite, limits, supervision, compensation, and internal controls work together to safeguard stability.

Through real-world examples and regulatory frameworks, the chapter emphasizes:

• The evolution from governance failures → risk-management failures → integrated oversight

• Board accountability and independence

• Formal risk appetite and limit-setting processes

• Tiered limit controls and escalation protocols

• Compensation reforms to curb excessive risk-taking

• Independence and rigor of the internal audit function

By the end of this chapter, you will understand not only what governance structures look like, but why they exist, how they interact, and how they are tested in global regulatory frameworks and real-world cases.

In other words — this chapter bridges policy, practice, and exam mastery, equipping you with both theoretical clarity and practical intuition for how risk is governed in modern financial institutions.

-

1. Risk Governance – from Vague Principle to Well Defined Best Practices

05:56 -

2. Global Post Crisis Regulatory Response – Basel 3

05:16 -

3. Dodd Frank Act

04:53 -

4. SREP and EBA Stress Test

02:52 -

5. Infrastructure of Risk Governance

06:20 -

6. Risk Appetite Statement

02:21 -

7. Risk Governance in Action

04:08 -

8. Incentives & Risk Taking

03:33 -

9. Assessing the Banks Audit Function

03:26

Chapter 4 – Credit Risk Transfer Mechanisms

This chapter offers a comprehensive and intuitively structured overview of credit risk transfer, credit derivatives, and securitization, integrating conceptual foundations with real-world historical developments. It consolidates the key topics tested in FRM Part I related to credit risk management, default risk, structured finance products, and risk-transfer mechanisms, giving candidates a deep and exam-relevant understanding of how modern financial markets redistribute credit exposure.

We begin with the fundamental problem at the core of banking credit risk: the mismatch between short-term liabilities (deposits) and long-term, illiquid assets (loans). This imbalance creates significant credit exposure, motivating the development of tools that isolate, hedge, and transfer default risk. The chapter examines the emergence of credit derivatives, particularly credit default swaps (CDS), which Alan Greenspan famously described as ushering in a new era of active credit risk management by enabling banks to offload credit exposures during periods of market stress.

To build a clear conceptual foundation, the chapter organizes the credit risk transfer universe into three FRM-important categories:

1. Credit Derivatives — such as CDS, where payoffs are triggered by credit events like default.

2. Securitized Products — including ABS, ABCP, MBS, CLOs, and CDOs, all backed by pools of loans or receivables.

3. Securitization Vehicles — including SPVs and SIVs, which legally isolate assets and issue securities.

Understanding these distinctions is essential for navigating the structured finance material in the GARP curriculum, as each class carries different implications for credit risk, liquidity risk, and counterparty risk.

The chapter then walks through the mechanics of securitization, explaining how loan portfolios are transferred to a Special Purpose Vehicle (SPV), aggregated into a diversified pool, and transformed into tranches — senior, mezzanine, and equity. This tranching structure redistributes default risk across investors. A critical FRM point emphasized is that the SPV is a pass-through entity: it issues the bonds but does not guarantee them. Investors fully bear the underlying credit risk, making tranche performance dependent on the quality of the collateral pool.

We then broaden the lens to examine the benefits and pitfalls of securitization, covering its role in:

• expanding funding capacity,

• transferring credit and liquidity risk,

• enhancing market liquidity, and

• improving capital efficiency.

But securitization also introduces moral hazard, as originators may underwrite with less discipline when they expect to transfer risk. This became a central issue before the 2007–2008 Global Financial Crisis, leading regulators to introduce the risk-retention (“skin-in-the-game”) requirement under Section 15G of the Securities Exchange Act, mandating that securitizers retain at least 5% of credit risk.

The chapter includes a historical overview of securitization markets, tracing their evolution from government-sponsored entities like GNMA, Fannie Mae, and Freddie Mac to large-scale private-label issuance in the 1990s and early 2000s. As securitization spread from the U.S. to the UK and continental Europe, the range of products expanded to include CLOs, credit card ABS, auto ABS, synthetic CDOs, and ABS-backed CDOs. A pivotal development was the explosive growth of subprime RMBS, which represented over 20% of all U.S. mortgage originations by 2006 — one of the major vulnerabilities in the structured finance ecosystem.

We then analyze what went wrong in 2007, emphasizing that the crisis stemmed not from securitization itself but from failures in underwriting standards, credit ratings, incentive structures, and risk governance. Instead of transferring risk under the originate-to-distribute model, banks became concentrated investors in securitized assets:

• 30% of AA-rated ABS were on their own balance sheets

• 20% were held via Structured Investment Vehicles (SIVs)

SIVs relied on short-term asset-backed commercial paper (ABCP) to fund long-term ABS, creating extreme maturity mismatch and rollover risk. When funding markets froze, sponsoring banks were forced to absorb the losses — proving that the risk transfer was incomplete and economically still on the books.

These breakdowns contributed to the self-reinforcing securitization chain, driven by misaligned incentives at the origination stage, opaque product structures, inflated credit ratings, and yield-driven investor demand. This combination amplified systemic vulnerability and culminated in a global liquidity collapse.

Despite these failures, securitization remains a foundational component of global credit markets. Post-crisis regulatory reforms, improved underwriting standards, and enhanced transparency have contributed to the continued resilience and relevance of structured finance markets, which remain substantial today.

Overall, this chapter gives FRM candidates a fully integrated understanding of:

• credit risk transfer mechanisms,

• the structure and purpose of CDS, ABS, MBS, CDOs, CLOs,

• the role of SPVs and SIVs,

• securitization mechanics and tranching,

• pre-crisis vulnerabilities and systemic failures,

• risk retention and post-crisis regulation, and

• the historical evolution of structured finance markets.

It is a holistic, exam-focused deep dive into one of the most important sections of the GARP FRM Part I curriculum, ensuring mastery of the terminology, mechanics, incentives, and risks that define modern credit markets.

-

1. Overview of Credit Risk Transfer Mechanisms

03:20 -

2. Key Terms in Credit Risk Transfer

02:44 -

3. Mechanics of Securitization

02:45 -

4. Credit Derivatives

04:25 -

5. Securitization Benefits & Pitfalls

03:41 -

6. Securitization – Historical Background

03:38 -

7. What went wrong in 2007

05:41

Chapter 5 – Modern Portfolio Theory and CAPM

This chapter provides a complete, intuitive, and exam-focused walkthrough of the core portfolio management frameworks tested in FRM Part I — including Modern Portfolio Theory (MPT), Mean–Variance Optimization (MVO), the Capital Market Line (CML), the Security Market Line (SML), the Capital Asset Pricing Model (CAPM), beta estimation, and the full suite of risk-adjusted performance measures used in professional portfolio evaluation. Across eight tightly structured video lessons, you will build a deep conceptual foundation while also learning the exact mechanics, formulas, and interpretations that appear frequently in GARP’s FRM exam.

1. Modern Portfolio Theory & Mean–Variance Optimization

You begin by learning how expected returns, standard deviations, covariances, and correlations feed into the MVO framework to construct the efficient frontier. Through numerical examples and intuitive explanations, you’ll see how asset allocation decisions shape portfolio risk and return — and why only the upward-sloping portion of the frontier is economically meaningful.You also explore the limitations of MVO, including estimation error, correlation breakdown (highlighted by Craig Israelsen’s findings), non-normal return distributions, and the sensitivity of MVO to input assumptions. Understanding these weaknesses is crucial for answering conceptual FRM questions.

2. Capital Market Line (CML) and Security Market Line (SML)

You will learn how introducing a risk-free asset transforms the efficient frontier and leads to the Capital Market Line, the Sharpe ratio, and Tobin’s Two-Fund Separation Theorem.Then, you move to the Security Market Line, which connects beta with expected return and is the key to understanding equilibrium pricing under CAPM. The differences between the CML (portfolio efficiency) and SML (security valuation) are core FRM test points.

3. CAPM and Beta

The chapter provides a complete breakdown of the Capital Asset Pricing Model, including:

• its historical origins with William Sharpe,

• the decomposition of risk into systematic vs. idiosyncratic,

• what beta measures, and

• why only systematic risk is priced in equilibrium.

You’ll learn both the regression-based (explicit) and covariance-based (implicit) methods of estimating beta — with an emphasis on the implicit formula, which is highly testable in FRM exams.

4. Risk-Adjusted Performance Measures

The chapter ends by integrating all concepts into performance evaluation using:

• Sharpe Ratio (total risk)

• Treynor Ratio (systematic risk)

• Jensen’s Alpha (regression intercept)

• Information Ratio (active return vs. tracking error)

You’ll understand how each measure works, what it captures, how to interpret it, and which risk measure (standard deviation vs. beta vs. tracking error) is used in each case.

⭐ Why This Chapter Matters for FRM Candidates

This chapter covers some of the most heavily tested topics in the FRM Part I exam, including:

• MPT & Efficient Frontier

• Mean–Variance Optimization

• Systematic vs. Total Risk

• CAPM, CML, SML

• Beta estimation & interpretation

• Risk-adjusted performance evaluation

Mastering these concepts will significantly improve your performance in the Portfolio Management and Quantitative Analysis sections of the FRM curriculum.

🔍 Keywords

FRM Part I, Modern Portfolio Theory, Mean–Variance Optimization, Efficient Frontier, Capital Market Line, Security Market Line, CAPM, Beta Estimation, Systematic Risk, Idiosyncratic Risk, Sharpe Ratio, Treynor Ratio, Jensen’s Alpha, Information Ratio, Tracking Error, Risk-Adjusted Performance, Portfolio Management, Quantitative Analysis, Asset Allocation, William Sharpe, Markowitz, Tobin, Risk–Return Tradeoff, Portfolio Construction.

-

1. Introduction

03:54 -

2. Modern Portfolio Theory – MVO Framework

05:46 -

3. Modern Portfolio Theory – Limitations & Use Cases

04:14 -

4. The Capital Market Line (CML)

05:31 -

5. Capital Market Line (CML) vs Security Market Line (SML)

04:53 -

6. The Capital Asset Pricing Model

04:51 -

7. Estimating Beta

06:00 -

8. Performance Measures

05:59

Chapter 6 – The Arbitrage Pricing Theory and Multifactor Models of Risk and Return

This chapter provides a complete, FRM-exam-focused treatment of asset pricing and multi-factor models, exactly as required for FRM Part 1 – Quantitative Analysis. The goal is not just to show formulas, but to help you understand how the models fit together, what is testable, and how to think under exam pressure.

We begin with a timeline-based overview of how asset pricing models evolved—from the single-factor CAPM, to Arbitrage Pricing Theory (APT), and finally to fully specified multi-factor models. This big-picture structure is critical for organizing the FRM curriculum and avoiding confusion between models that look similar on the surface but differ conceptually.

You will then develop a deep intuition for Arbitrage Pricing Theory, including systematic vs. idiosyncratic risk, zero-beta portfolios, factor risk premiums, and the most important exam takeaway: why a zero-beta portfolio cannot earn a positive excess return. The chapter clearly explains why APT is a pricing theory rather than a fully specified model, a distinction that is frequently tested.

From there, the chapter moves into multi-factor models, breaking them into the three categories used throughout the FRM curriculum:

• Macroeconomic factor models (Chen–Roll–Ross; Burmeister–Ibbotson–Roll–Ross)

• Fundamental factor models (Fama–French, Carhart, Fama–French five-factor model)

• Statistical factor models (Principal Component Analysis)

Each category is explained at exactly the level required for the exam, with a strong emphasis on specified vs. unspecified factors, one of the most common conceptual traps in FRM questions.

A major portion of the chapter is dedicated to fundamental factor models and numerical interpretation, where many candidates lose points. You will work through exam-style regression examples, learning how to:

• Interpret factor loadings correctly

• Combine coefficient signs with factor behavior (SMB, HML, momentum)

• Ignore statistically insignificant variables safely

• Distinguish between backward-looking estimation and forward-looking expected return calculations

• Avoid common FRM traps involving alpha, betas, and p-values

The chapter also covers statistical factor models using PCA, with a concrete yield-curve example that builds intuition for level, slope, and curvature—exactly how this topic is tested in the FRM exam.

Finally, you will see how factor models are used for hedging, not just return explanation. This includes zero-beta and partial hedges, rebalancing trade-offs, transaction costs, model risk, and why market-neutral strategies can fail during crises—key insights that GARP increasingly emphasizes.

Throughout the chapter, the focus remains on:

• What is testable

• Why it works

• How exam questions are structured

• How to avoid losing easy points

This chapter is part of a fully visual, intuition-driven, exam-focused FRM course designed to help you master the curriculum efficiently and confidently.

👉 If you are preparing for FRM Part 1 and want a course that explains why things work—not just what to memorize—this chapter gives you exactly what the exam expects.

FRM, FRM Part 1, GARP FRM, Financial Risk Manager, FRM Quantitative Analysis, Asset Pricing Models, CAPM, APT, Arbitrage Pricing Theory, Multi Factor Models, Fama French, Carhart Model, PCA FRM, Factor Hedging, Risk Management, FRM 2025

-

1. Introduction

03:20 -

2. Arbitrage Pricing Theory (APT)

05:37 -

3. Multi Factor Models (Big Picture)

03:02 -

4. Macroeconomic Factor Model

02:35 -

5. Fundamental Factor Model

03:37 -

6. Fundamental Factor Model (Numerical Example 1)

07:12 -

7. Fundamental Factor Model (Numerical Example 2)

05:22 -

8. Fundamental Factor Model (Numerical Example 3)

04:27 -

9. Statistical Factor Models

05:09 -

10. Factor Analysis in Hedging Exposure

04:43

Chapter 7 – Principles for Effective Data Aggregation and Risk Reporting

This chapter provides a comprehensive, FRM exam–focused explanation of BCBS 239, officially titled the Principles for Effective Risk Data Aggregation and Risk Reporting (RDARR), a core regulatory framework emphasized throughout the GARP FRM curriculum. BCBS 239 is highly relevant for both FRM Part I and FRM Part II, particularly within readings on risk governance, operational risk, data management, and post-crisis regulatory reforms.

The chapter begins by establishing the importance of risk data aggregation, a foundational concept for FRM candidates. Using intuitive analogies and exam-relevant framing, it emphasizes that risk analysis is only as good as the data behind it, linking data quality directly to model input risk and the classic FRM principle of “garbage in, garbage out.” The distinction between internal and external risk data, along with the challenges posed by organizational silos and fragmented systems, explains why risk data aggregation became a regulatory priority following the global financial crisis.

Building on this foundation, the chapter introduces BCBS 239 in its historical and regulatory context, explaining what the framework is, why it was introduced, and how it fits into the broader Basel and post-crisis regulatory landscape tested by GARP. Key milestones—including the 2013 publication, the missed 2016 implementation deadline, and subsequent BCBS 239 progress reports issued by the Bank for International Settlements—are discussed to highlight persistent industry-wide compliance challenges. Particular emphasis is placed on exam-relevant insights such as underestimated implementation complexity, the premature application of advanced analytics on fragmented data, and the regulatory expectation that BCBS 239–compliant data must support both internal risk management and regulatory reporting, as emphasized by the European Central Bank.

The chapter then presents a clear structural overview of the BCBS 239 framework, breaking down the 14 principles across four categories:

1. Governance and infrastructure,

2. Risk data aggregation capabilities,

3. Risk reporting practices, and

4. Supervisory review, tools, and cooperation.

Each category is explored with a strong FRM exam orientation, focusing on intuition, testable takeaways, and conceptual clarity rather than regulatory wording. Governance principles emphasize board and senior management responsibility, resource allocation, and awareness of data limitations. Risk data aggregation principles focus on accuracy, integrity, completeness, timeliness, and adaptability, including automation, reconciliation to source systems, and the ability to support ad-hoc stress testing. Risk reporting principles highlight clarity, usefulness, frequency, and coverage of both Pillar 1 and Pillar 2 risks, while supervisory principles complete the framework by explaining ongoing supervisory review, remedial actions, and home–host cooperation for internationally active banks and G-SIBs.

The chapter concludes by connecting FRM theory with real-world BCBS 239 compliance outcomes, analyzing industry compliance assessments across multiple years. These results illustrate that while progress has been made, full compliance remains elusive, reinforcing why BCBS 239 continues to be actively monitored by supervisors and repeatedly tested in the FRM exam.

Overall, this chapter is designed specifically for GARP FRM candidates, helping you understand what BCBS 239 is, why it matters, how it is applied in practice, and how it is tested. The focus throughout is on building intuition, reinforcing exam-relevant concepts, and reducing unnecessary memorization for one of the most important regulatory frameworks in the FRM syllabus.

-

1. The Importance of Data Aggregation

03:32 -

2. BCBS 239 – Background

04:40 -

3. BCBS 239 – Overview or Principles

03:04 -

4. BCBS 239 – Principle 1,2

03:40 -

5. BCBS 239 – Principle 3,4,5,6

02:40 -

6. BCBS 239 – Principle 7,8,9,10,11

02:39 -

7. BCBS 239 – Principle 12, 13, 14

01:52 -

8. BCBS 239 – Compliance

02:50

Chapter 8 – Enterprise Risk Management and Future Trends

This chapter provides a structured, intuition-first introduction to Enterprise Risk Management (ERM) as taught in the FRM Part 1 curriculum by GARP. Instead of treating ERM as a list of definitions, we build a coherent enterprise-wide risk mindset: why firms need ERM, how it differs from siloed risk management, how modern ERM evolved after the Global Financial Crisis, and why qualitative elements like risk culture, judgment, and behavioral biases often determine whether ERM works in practice. The goal is to help FRM candidates develop the kind of conceptual clarity that exam questions test—especially on governance, scenario analysis, stress testing, and enterprise-wide risk oversight.

We begin by defining ERM as a holistic framework that manages risk at the enterprise level, rather than in isolated business-unit silos. This chapter emphasizes why siloed views hide both diversification effects and risk concentrations, while a unified ERM approach makes interactions visible and supports consistent risk appetite, firm-wide oversight, and better aggregation of exposures. The intuition is reinforced using the Northern Rock case study, where a UK mortgage lender relied heavily on wholesale funding while lending long-term to households—an enterprise-wide fragility that became fatal when liquidity dried up in 2007, triggering a bank run and eventual nationalization. This real-world failure makes the ERM message concrete: risks rarely stay contained inside one “box,” and weak enterprise oversight can turn a business model into a liquidity crisis.

Next, we place ERM on a simple historical timeline to explain why modern frameworks look the way they do today. The story starts with the postwar financial system and the shift from the stability of Bretton Woods to the higher volatility environment that followed market liberalization and floating exchange rates. Early corporate risk management focused heavily on risk transfer via insurance, but over time firms moved toward risk retention, including self-insurance and captive insurance, reflecting the core idea that risk cannot be managed if it is not understood—and it cannot be fully understood if it is entirely transferred away. The chapter then explains how ERM formalized in the 1990s with the rise of the Chief Risk Officer (CRO) role, firm-wide risk divisions, and risk metrics such as Value at Risk (VaR). Importantly, the Global Financial Crisis exposed the limitations of a purely metric-centric approach, accelerating the shift toward a scenario-centric ERM framework built on stress testing and forward-looking vulnerability analysis.

We then translate ERM from “vision” into an actionable framework using the curriculum’s five ERM dimensions: targets (risk appetite), structure (governance and oversight), metrics (risk measurement such as VaR), ERM strategies (execution and management actions), and culture (tone at the top and risk mindset). A key intuition is that the first four form the “bones” of ERM, while culture is the flesh—meaning ERM effectiveness depends on how these dimensions interact, not on any single policy or model. We also explain why firms demand ERM in practice: ERM creates top-to-bottom vertical vision that links local risk-taking to firm-wide outcomes, identifies hidden concentration risk (geography, product, industry, supplier), captures cross-risk interactions across market, credit, and operational risk, and supports intentional risk retention rather than blind transfer.

A dedicated section focuses on risk culture, because ERM succeeds or fails largely through behavior, incentives, and governance. Risk culture is defined as the values and norms that shape how risk-taking and risk management actually occur, including the firm’s real tendency to follow best-practice risk management—not just what is written in policies. We discuss how regulators and practitioners assess risk culture using indicators often associated with the Financial Stability Board, including accountability, effective communication and challenge, incentives, and tone from the top, alongside broader qualitative signals such as escalation practices, whistleblowing, risk literacy, and responses to incidents. We also highlight why risk culture is difficult: it’s hard to quantify, easy to “fake,” often measures direction rather than financial impact, and tends to form locally at the desk, team, or business-line level rather than being imposed centrally.

The chapter then builds precise conceptual clarity around sensitivity testing, scenario analysis, stress testing, and reverse stress testing, using a simple cause–effect framework. Sensitivity testing changes one risk driver at a time, scenario analysis allows multiple drivers to move together, and stress testing is scenario analysis focused on severe but plausible conditions. Reverse stress testing flips the logic: it starts from a defined failure outcome—such as insolvency or a bank run—and works backward to identify what combination or magnitude of shocks could cause it. This cause-to-effect versus effect-to-cause framing helps FRM candidates answer conceptual exam questions consistently.

Finally, we tie the scenario-centric shift to post-crisis regulation and explain how stress testing requirements shaped modern ERM in the U.S. and Europe. In the United States, Dodd–Frank introduced stress testing frameworks such as DFAST and CCAR, while Europe developed comparable supervisory approaches such as SREP. We explain how U.S. stress testing differs by bank size (small, medium, large), why CCAR is more demanding through its capital plan requirement, and how predefined baseline/adverse/severely adverse scenarios encourage consistent benchmarking across institutions. We also introduce contingent convertible bonds (CoCos) as post-crisis capital instruments that absorb losses through conversion or write-down once triggers are breached, illustrating how ERM, stress testing, and capital structure connect in practice. We also contrast today’s dominant deterministic scenario testing with the forward-looking idea of stochastic scenario testing, where thousands of scenarios could be simulated and expanded beyond macro variables into areas such as geopolitical risk.

The chapter closes by confronting the reality that ERM is difficult even when the framework looks perfect on paper. Enterprise risk emerges from interactions, not isolated categories, and firms face not only measurable risk but also ambiguity, where outcomes are conceivable but probabilities are unknown (pandemics, geopolitical shocks). The reading’s lessons from the Global Financial Crisis reinforce why third-party ratings cannot substitute for internal judgment and why the CRO must be involved in growth and strategy—not just controls. We then show why judgment introduces behavioral distortions by reviewing key behavioral biases (anchoring, framing, groupthink, herding, loss aversion, mental accounting, and more) that systematically push decision-making away from rational models. The central takeaway is that ERM is a practical discipline that sits at the intersection of measurement, governance, culture, and human behavior—and when implemented poorly, it can create a false sense of security rather than real resilience.

FRM, Financial Risk Manager, FRM Part 1, GARP, Enterprise Risk Management, ERM, holistic risk management, siloed risk management, risk appetite, risk aggregation, risk concentration, diversification effects, correlation, risk culture, tone at the top, incentives, accountability, Financial Stability Board, scenario analysis, sensitivity testing, stress testing, reverse stress testing, deterministic scenario testing, stochastic scenario testing, Value at Risk, VaR, Global Financial Crisis, Dodd-Frank Act, DFAST, CCAR, SREP, capital planning, contingent convertible bonds, CoCos, Chief Risk Officer, CRO, risk transfer, risk retention, captive insurance, self-insurance, behavioral biases, ambiguity premium, Brenner and Izhakian, Northern Rock, funding liquidity risk, bank run, FRM exam preparation.

-

1. ERM – What it is and why Firms need it

04:41 -

2. ERM – Brief History

04:39 -

3. ERM – From Vision to Action

06:18 -

4. Risk Culture

04:50 -

5. Sensitivity Testing, Scenario Analysis, Stress Test & Reverse Stress Test

03:48 -

6. Scenario Centric ERM Approach – US & EU Regulation

05:05 -

7. Dodd Frank Act – DFAST & CCAR

05:03 -

8. ERM – Challenges

06:26

Student Ratings & Reviews

No Review Yet